Register with CAA to get access to the CBAM portal as soon as possible, you will have time to submit the reports you missed until the end July 2024.

To request a delay submission for the first time, click on the ‘Request Delay’ button on the right of the Quarterly Report you need to submit and indicate ‘Requested by Declarant (technical error)’. The request is approved automatically.

In order to request for successive delays, please, follow the steps outlined below:

1. Access the CBAM portal through this link: https://cbam.ec.europa.eu/declarant/

2. Go to ‘Requests’

3. Click on ‘Create Request’

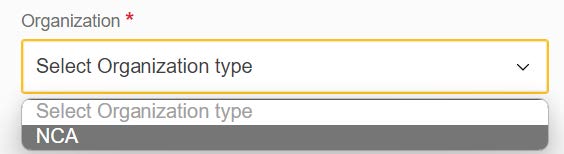

4. Select ‘NCA’ in the Organization field

5. As a Title use ‘Request delayed submission for QX YYYY’ where X is the quarter number and YYYY is the year of the reporting period you need to complete.

6. For the type of request select ‘Request for Information/Documents’

7. Priority medium

8. The due date should be one week from the day of the request.

9. In the message mention that you request a delayed report submission for QX YYYY giving a reason for the delay and listing your details including i) Company name ii) EORI number iii) Name and Surname iv) ECAS email and username

10. Then click on ‘Create Request’, on the top right side of the page.

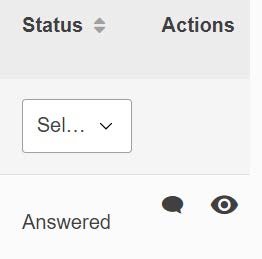

We will then process your request from the system. Once the request is received and a reply is provided, the status will change to ‘Answered’ and you can then see the reply by:

11. Access the CBAM portal through this link: https://cbam.ec.europa.eu/declarant/

12. Go to ‘Requests’

13. Click ‘Outgoing’

14. Click on the eye icon at the right side of the request

15. Scroll down to the Response where you will receive a reply with the reference number.

Once you have the reference number you can go back to ‘My Quarterly Reports’ and ask for a delay using that reference number.

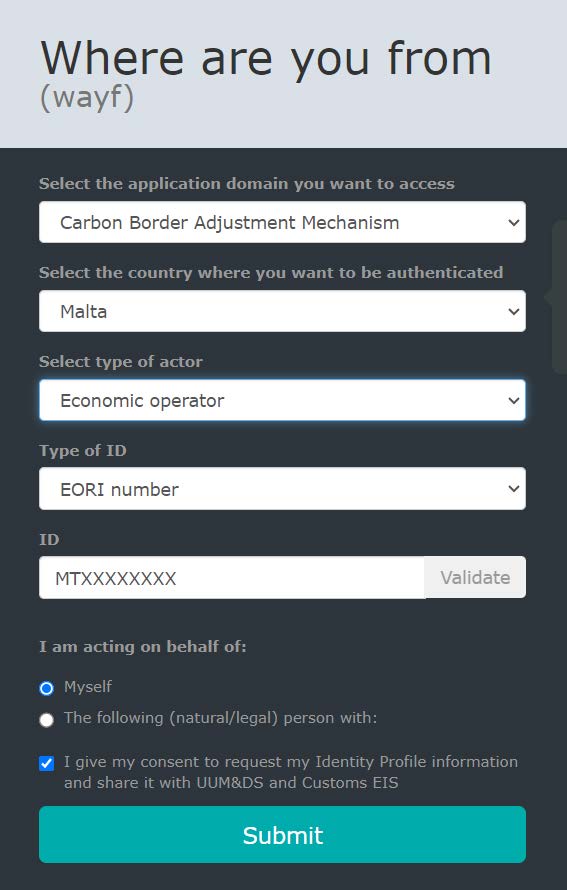

Please make sure that you are trying to access the right portal:

PRODUCTION (Official) https://cbam.ec.europa.eu/declarant/ for the actual report

CONFORMANCE (Testing) https://conformance.cbam.ec.europa.eu/declarant for testing the portal.

Also, make sure you select the proper ‘Type of actor’, which can be either ‘Economic operator’ or ‘Customs representative’.

In the ID field enter the EORI (VAT) number with no spaces nor dashes. Select ‘I am acting on behalf of:’ ‘Myself’ and tick the last box.

Finally, click ‘Submit’.

Sometimes the system memorises the wrong access information provided and, as a result will deny your access. In this case, clean the browser cache and restart the browser. If this doesn’t work, try restarting the computer.

Moreover, the website may also not respond correctly due to maintenance and/or update.

If the issue persists, please contact us at cbam.caa@climateaction.gov.mt

The commission has developed a Communication Template to facilitate the exchange of information required for you to submit the CBAM Report. Please note, that this document is solely for you and your manufacturer, and it is not valid as report. The data from the last three tabs (Summary Processes, Summary Products, Summary Communication) will need to be transferred to the CBAM portal manually. There is currently not guidance available on the communication template – official guidance from the Commission should become available by end of year. Having said that, the NCA is preparing the necessary training to be delivered soon.

The Commission is preparing guidance documents in various languages. Kindly keep an eye out for these on the Commission’s CBAM webpage, under the Guidance section: Carbon Border Adjustment Mechanism – European Commission (europa.eu). Versions in languages other than English are being made available.

The Commission has published Default Values for the transitional period which can be used instead of the actual supplier data that you need to get through the communication template. However, these default values can only be used until the end of July 2024. After that, actual manufacturer data will be required.

Please note that this regulation is relatively new for everyone, and some suppliers may still be unaware of it. However, if they provide CBAM goods to other European importers, then they will need to furnish this information to other importers.

You should get your data either through your distributor (which will need to contact the manufacturer himself) or by contacting the manufacturer yourself (for this you will need to ask the distributor to provide you with their contact information).

In the list of Import Procedures you can find the description of each type. The import procedure is also indicated in the customs declaration. If you are still unsure, please contact Customs to identify which import procedure applies to your imports.

In the CBAM portal, you are able to report imports of the same CN code under one item. You will however need to specify the different Country of Origin, import procedures and net mass (and unit) on the Goods Imported page (by clicking the Add new button just above the first grey box, and on the Emissions Section (by clicking on the Add an Emission button displayed on the left-hand side of the screen). You should have the same number of emission entries as you had specified in the Goods Imported Section.

If you have imported the same CN code from the same country but from different suppliers, and you are reporting using default values, you will be able to enter all the emissions as a sum into one Emissions Tab. This is applicable only during the Transitional Period and when using Default Values.

In the portal, you must select the code from the dropdown list after you input the first 4 digits, otherwise it will give an error. If the CN code is in the CBAM Regulation list but is not showing on the portal, you should report this issue to us for further action on cbam.caa@climateaction.gov.mt.

From 2025, the Commission will be registering Operators of installations in Third Countries. The list of operators of installation will become available as a drop-down menu in the Installations Tab of the CBAM portal. CBAM declarants will have the opportunity to choose the relevant operators from that list – this will, however, become available at a later stage (late 2025-2026). Since this functionality is not yet available, the information on the operators/installations is not mandatory.

For the time being, leave this section empty and make sure to delete any fields related that were opened.

No, if you have not imported any CBAM goods during that particular quarter, you should not report anything.

We appreciate the difficulties you are encountering, and we are working with the Commission to facilitate the process.

MRA is also organising online and in-person workshops demonstrating how to report using the CBAM Portal.

For specific issues you can contact us at cbam.caa@climateaction.gov.mt

If you notice that you have missed reporting an import during a quarter whose reporting period has elapsed, you might not be able to amend your report, as the reporting portal for reporting quarters closes once the reporting period is over. If you had requested a delay for that quarter, you might however be able to do so. You will need to check if you are able to amend your report by clicking on the report number in blue and check whether you have an Amend button at the top. For future reports, kindly make sure to submit correct reports, as amendments will not be possible after the report submission deadline.

Once the review has been carried out by the Commission, importers will also be notified in case of incorrect/incomplete data and will have the chance to rectify the report accordingly, at that stage.

The temporary admission procedure is not in the scope of CBAM and not considered an import as per CBAM provisions. Hence, such goods shall not be reported under CBAM. Goods are in scope of CBAM when they are not re-exported after their usage and are declared for free circulation. In this case, such goods must be reported in the CBAM report.

You must always use the data entered in the Customs declaration. The Commission will be conducting reviews and cross-checking the information you have entered on the CBAM portal with the information of the Customs Declarations. Make sure that the commodity codes reported on the customs declaration are correct.

All goods falling within scope of CBAM, imported during a certain quarter, will all need to be reported in a single report.

For instance, goods falling under the CBAM Regulation, imported between January and March 2024, will all have to be reported in the Q1 2024 Report.

Currently, this functionality is not available on the CBAM portal. However, you can download a copy of the submitted report as .pdf and split it using an online PDF splitter.

In cases where couriers are lodging customs declarations for you, ensure that they specify the correct item price (excluding shipping price) on the customs declaration form.

The EU customs legislation and hence the customs import system (NIS) allow a declarant to declare value either as C&F (cost and freight) or FOB (freight on board) indicating that the transport charge is included in the freight charges field.

The item price (box 42) excludes shipping cost. The statistical value (box 46) includes shipping cost. If the invoice does not include the item price (i.e. excluding shipping), the courier will not be able to report the item price (without shipping).

If you import goods from non-EU countries, to be assembled in Malta and then exported/released into other EU countries for free circulation, your goods will fall under the inward processing procedure, and customs import procedure 4000000 (aka ‘four million’). When reporting the import of the goods being used for such purposes, on the CBAM portal, you will need to report them under Import Procedure 40 and tick the box ‘Inward Processing’.